SMM January 2 News:

Key Points: This week (December 26-31, 2025), the solid-state battery sector saw multiple breakthroughs in capital, capacity, applications, and standards. On the industry side, the signing of leading projects, the commissioning of GWh-level production lines, and the delivery of semi-solid-state vehicles marked an acceleration in industrialisation. Technologically, innovations such as sulphide electrolytes, composite functional layers, and sodium-ion batteries continued to emerge. In terms of policy, the drafting of the first national standard for vehicle use laid the foundation for the industry's standardized development, with the industry chain ecosystem becoming increasingly mature.

This week's developments collectively reflect a comprehensive leap from "lab-bench-pilot-production" for the solid-state battery industry. The enthusiasm of capital, the realization of capacity, and the initiation of the first national standard together constitute key signals for the industry's move towards large-scale expansion.

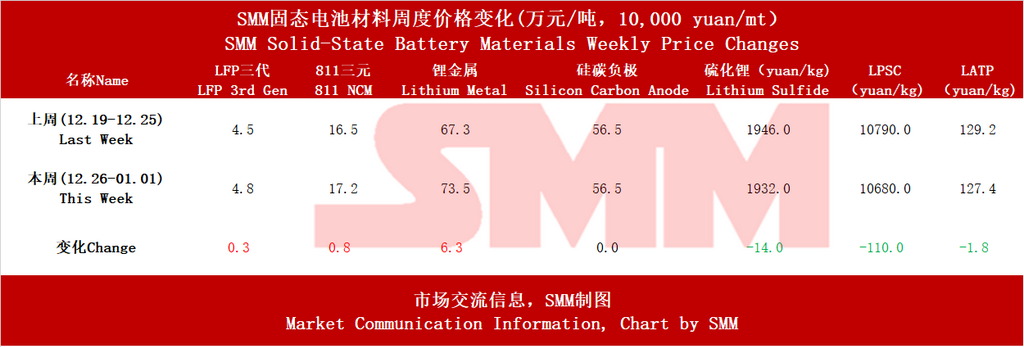

Preface: Weekly price situation. Prices for cathode materials in the solid-state battery industry have risen, while lithium metal anodes have increased and silicon-carbon remains stable. The prices of solid-state battery-specific materials, such as lithium sulfide and electrolytes, have decreased.

I. Progress in Material Systems: Electrolytes and Key Materials Become the Focus of Innovation

Sulphide Route: The Wuxi Huishan project team focused on optimizing the interface of sulphide electrolytes and the preparation of ultra-thin films, which are core challenges for achieving high-energy-density all-solid-state batteries. Jinyang High-Tech applied for a patent on the preparation of high-purity lithium sulfide, aiming to improve purity and reaction efficiency at the raw material end, thereby reducing the cost of large-scale production.

Polymer/Composite Route: CATL's new patent focuses on polymer-based composite functional layers, enhancing the cycle stability of solid-state batteries by introducing specific-sized graphene materials, demonstrating the deep optimization of mainstream producers on incremental technology routes. Taland New Energy's "oxygen-polymer composite" route and Xinjie Energy's "HICORE" solid-state electrolyte technology both represent differentiated innovation in the electrolyte material system.

High-Energy Trend: The new manganese-based cathode material used in the semi-solid version of the MG4 has been independently produced and installed. Zhaona New Energy's all-solid-state sodium-ion battery, using atomically designed layered oxide cathodes, achieves an energy density of 348.5 Wh/kg, breaking through the limitations of traditional sodium-ion batteries and showcasing the significant potential of cathode material innovation.

Application of Lithium Metal Anodes: Xinjie Energy achieved GWh-level mass production of solid-state lithium metal batteries, and Zhaona New Energy adopted an "anode-free" structure, both pointing to the ultimate solution for increasing energy density, but currently mainly targeting high-end consumer electronics and specific fields.

II. Battery Cells and Battery Systems: Comprehensive Industrialization

This week saw a flurry of capacity announcements: Xinjie Energy (2GWh) began mass production, Luochu Technology (2GWh) started construction, and Taland New Energy secured over 400 million yuan in financing to advance industrialization. Diversified capacity layouts are emerging across consumer electronics, low-altitude economy, and power storage.

Wuxi Huishan introduced a full solid-state battery headquarters and pilot base, and Del Co. achieved continuous trial production, indicating that the industry is moving steadily from cutting-edge R&D to engineering and consistent manufacturing.

Product Diversification and Application Expansion

Applications now extend far beyond EVs: Zhonggu Times released large-capacity products for ESS (Taihang No.1) and integrated power and storage (Taihang No.2); Luochu Technology focuses on high C-rate semi-solid-state batteries for drones and special equipment; Narada Power, Del Co., and Xinjie Energy are all expanding into robotics, drones, and consumer electronics. The delivery of SAIC MG4's semi-solid model marks the first mass production milestone in the power sector.

III. Supporting Systems and Industry Ecosystem

Equipment and Capital: Equipment company Yugong High-Tech received funding, specializing in solid-state battery production equipment, a critical link in the maturation of the industry chain.

Local industrial funds (such as Wuxi Huishan) are actively being established to drive regional cluster development through capital.

Standards and R&D Collaboration: The most significant event was the public solicitation of comments on the first national standard for "Solid-State Batteries for Electric Vehicles," which will end market concept chaos and establish a unified benchmark for product testing, evaluation, and market entry, a necessary condition for the industry's maturity.

Jinhé Industry and universities jointly established a laboratory, focusing on the R&D of upstream materials such as lithium sulfide and specialized adhesives, deepening the integration of industry, academia, and research.

IV. Summary and Outlook

This week's developments paint a clear picture of the industry: a multi-route technological competition, a multi-scene application explosion, and dual-driven capital and policy. Semi-solid-state batteries have already achieved a commercial loop from GWh-level capacity to vehicle delivery, while the path to industrialization for all-solid-state batteries is becoming clearer with material breakthroughs, pilot line construction, and standard leadership. With the formulation of the first national standard, the industry will move away from disorderly speculation and enter a new phase of standardized, rapid development, with product performance, cost, and reliability as the core competitiveness.

According to SMM forecasts, all-solid-state battery shipments will reach 13.5 GWh by 2028, while semi-solid-state battery shipments will reach 160 GWh. Global lithium-ion battery demand is projected to reach approximately 2,800 GWh by 2030, with the EV sector's lithium-ion battery demand showing a CAGR of around 11% from 2024 to 2030, ESS lithium-ion battery demand at a CAGR of about 27%, and consumer electronics lithium battery demand at a CAGR of roughly 10%. Global solid-state battery penetration is estimated at about 0.1% in 2025, with all-solid-state battery penetration expected to reach around 4% by 2030, and global solid-state battery penetration potentially approaching 10% by 2035.

**Note:** For further details or inquiries regarding solid-state battery development, please contact:

Phone: 021-20707860 (or WeChat: 13585549799)

Contact: Chaoxing Yang. Thank you!